16 Jul 2026

October deadline is looming for charity governance reviews

Charities have until October 2026 to complete a formal review of their governance procedures – and...

There is no doubt about it – things are heating up in the climate change arena, with New Zealand leading the way in setting climate reporting standards.

Time to read: 5 mins

In October 2021, the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Bill was passed and received Royal Assent. As a result, the External Reporting Board (XRB) now has a mandate to issue climate standards as part of a disclosures framework. These require some 200 of New Zealand’s top “climate-reporting entities” to disclose the impact climate change is having on their businesses, both now and into the future.

It would be fair to say that there are a plethora of standards, organisations and acronyms in the climate-reporting space so it’s worth developing an understanding of what these are.

The good news is that the XRB is basing the New Zealand standards on the “Taskforce on Climate-Related Financial Disclosures” (TCFD) framework, which outlines recommended disclosures across four key pillars: Governance, strategy, risk management, and metrics and targets.

Following closely behind New Zealand is the newly established International Sustainability Standards Board (ISSB), vice-chaired by Kiwi, Sue Lloyd. This Board was set up following the United Nations COP26 summit held in Glasgow last November and has already issued two exposure drafts on climate- and general sustainability-related financial disclosures.

The standards released by the ISSB will be part of the International Financial Reporting Standards (IFRS) suite and will apply for all countries that have adopted IFRS.

Other good news is that the XRB is closely monitoring the ISSB’s activities so the New Zealand standards will be as much aligned with international requirements as possible (given they are being developed ahead of international standards).

Australia has recently released its guide Developing sustainability-related financial reporting standards in Australia. The Australian Accounting Standards Board aims to use the work of the ISSB as the baseline for its work on sustainability-related financial reporting.

The UK government is also active in this space and has developed a Sustainability Disclosure Requirements (SDR) and investment labels road map that aims to bring together existing and new sustainability-related disclosure requirements in a single, integrated framework. This would be helpful for entities seeking to make sense of the different frameworks and requirements.

Climate-reporting entities are defined as “all registered banks, credit unions, and building societies with total assets of more than $1 billion, and all managers of registered investment schemes (other than restricted schemes) with greater than $1 billion in total assets under management”.

So essentially businesses at the big end of town with significant funds under management.

However, all entities that prepare IFRS-compliant financial statements are required to disclose the key impacts on their business, including information about assumptions that have a significant risk of resulting in a material change to the carrying amounts of assets and liabilities[1]. All other entities are encouraged to follow best practice in this area.

The XRB is developing the following three standards outlining the requirements:

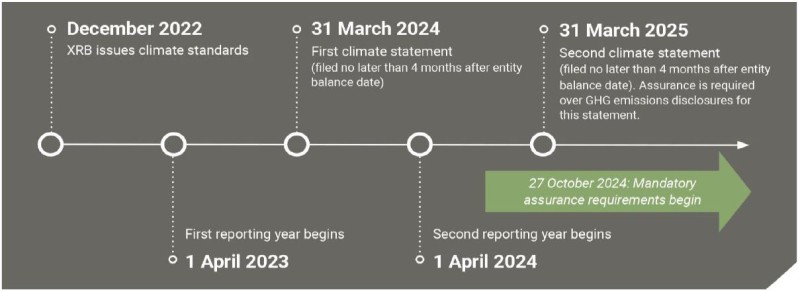

Soon! The XRB’s standards are due to be released by December 2022 and climate-reporting entities must report against the standards from 1 January 2023 onwards (i.e. entities with a 31 December year end prepare their first climate statement for the 31 December 2023 year and those with a 31 March, 30 June or 30 September year end will prepare their first climate statement as part of their 2024 annual reports).

When does reporting start? Example timeline for an entity with a 31 March balance date. Source: Aotearoa New Zealand Climate-related Disclosures Director Preparation Guide May 2022

This is a very common question and is where scenario analysis comes in. The XRB is encouraging entities in the same sector or industry to work together and agree on some possible scenarios (such as water levels rising by five metres or the temperature rising by 1.5%). The next step is to consider what impact this scenario might have on your business. If you’re not sure, that’s okay, you can make some assumptions about potential changes in consumer behaviour or government regulations and include these assumptions in your report.

The XRB has developed guidance on undertaking scenario analysis Disclosures – Scenario Analysis: Getting Started at the Sector Level and the TCFD has produced a six-step scenario analysis process that includes simple process steps and guidance on key assumption choices.

The key message is, if you have been burying your head in the sand hoping that this will all go away, it won’t. Providing information on how your business is impacting (and being impacted by) climate change and what you are doing to respond enables stakeholders to make well-informed decisions about where they spend and invest their money, time and other resources.

Doing so also helps demonstrate accountability and foresight in relation to climate-related risks and opportunities, and “shines the light” on action being taken by businesses to transition to a more sustainable low-emissions economy.

[1] Para 125 of NZ IAS 1 Presentation of Financial Statements available at: www.xrb.govt.nz/standards/accounting-standards/for-profit-standards/standards-list/nz-ias-1/

DISCLAIMER No liability is assumed by Baker Tilly Staples Rodway for any losses suffered by any person relying directly or indirectly upon any article within this website. It is recommended that you consult your advisor before acting on this information.

Our website uses cookies to help understand and improve your experience. Please let us know if that’s okay by you.

Cookies help us understand how you use our website, so we can serve up the right information here and in our other marketing.