15 Jun 2026

Tax Talk: GST Act in line for timely repairs and maintenance

New Zealand’s unwieldy GST Act has been overdue a tune-up – and proposals that have just been released...

The modernised and improved Incorporated Societies Act 2022 is finally here, replacing the 1908 Act that regulated incorporated societies for more than 110 years. Let’s break it down with our experts Nicola Hankinson and Rene Lamprecht…

Time to read: 4 mins

If you are one of the 24,000 not-for-profit entities registered as an incorporated society in New Zealand, you will no doubt be interested in what changes have been made, how they will impact you and what actions you should take.

Existing societies will continue to operate under the 1908 Act until they re-register under the 2022 Act or by 1 December 2025 at the latest. Failing to re-register by the transition date may result in the incorporated society ceasing to be registered.

So what are the key changes?

At least 10 members are now required to register an incorporated society (15 were required under the old Act). The society must have at least 10 members at all times. People will need to consent to become a member, and a Membership Register must be maintained and include specified minimum data.

Each society must have a committee comprising three or more qualified officers. A majority of those officers must be members of the society and/or representatives of corporate bodies that are members of the society. This committee will be the ”governing body of the society”, responsible for the management of its operations and affairs.

The criteria for who will qualify to be an officer of a society are set out in section 47 of the new Act. The officers must be:

The officers’ duties are also defined in the Act (sections 54-61) and are very similar to the duties of company directors. Officers must adhere to the following duties, which are owed to the society as opposed to its members:

Procedures for resolving disputes and other grievances between members, as well as between members and the society, must be documented and set out in the constitution. The society’s rules need to include certain provisions, for example nominating a not-for-profit entity to which surplus assets are given if the society winds up.

An annual return is required in a manner prescribed by the regulations (unless the society is also a registered charity, in which case the requirements of the Charities Act 2005 apply).

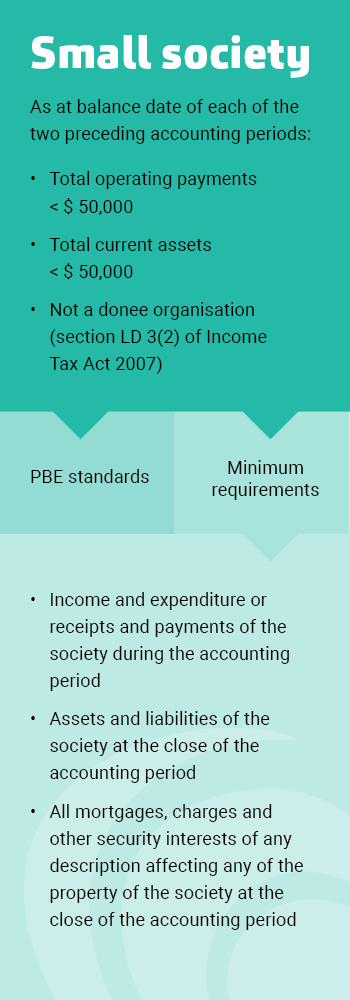

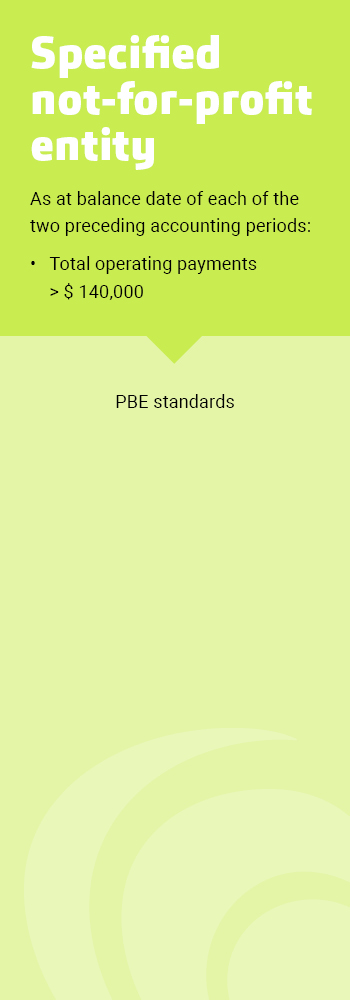

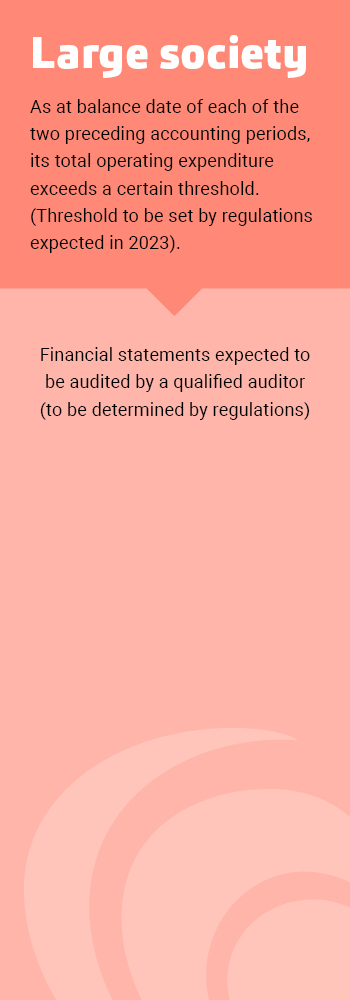

Every society must file financial statements with the registrar within six months after the balance date of the society.

The size of the society determines which accounting standards must be used to prepare financial statements. Currently many incorporated societies are preparing special purpose financial statements. They will now be required to prepare financial statements based on PBE reporting standards following registration under the 2022 Act, as outlined in the graphic at the bottom of this article. This may mean your society is required to prepare non-financial performance information for the first time. Larger societies will need to have their financial statements audited by a qualified auditor.

Two or more societies may also now amalgamate as one with the new amalgamation process set out in the Act. The resulting society may continue as one of the amalgamated societies or as a new society.

The Act also sets out criminal offences including making false statements, fraudulent use or destruction of property, falsification of the register, records or documents; operating fraudulently or dishonestly incurring debt, improper use of “Incorporated”, “Inc” or “Manatōpū”, banning order contravention, and infringement offences.

Now is a good time to review your society’s existing constitution and make the necessary modifications to ensure that it will comply with the requirements of the 2022 Act. Consideration should also be given to whether officers meet the eligibility criteria set out in Section 47 of the new Act.

Don’t know where to start? Don’t worry, help is at hand. At Baker Tilly Staples Rodway we can help you assess your financial reporting obligations and provide advice and assistance on complying with the 2022 Act. We have also prepared an Information Sheet (below) that you can use as a basis to work through the requirements and key changes.

Contact your usual advisor or our technical team technical@bakertillysr.nz

Our website uses cookies to help understand and improve your experience. Please let us know if that’s okay by you.

Cookies help us understand how you use our website, so we can serve up the right information here and in our other marketing.