15 Jun 2026

Tax Talk: GST Act in line for timely repairs and maintenance

New Zealand’s unwieldy GST Act has been overdue a tune-up – and proposals that have just been released...

Employee share schemes have long been a favourite of the technology sector because they allow key employees to be rewarded without a cash cost and allow those employees to be rewarded for helping to build the future value of the business.

Time to read: 5 mins

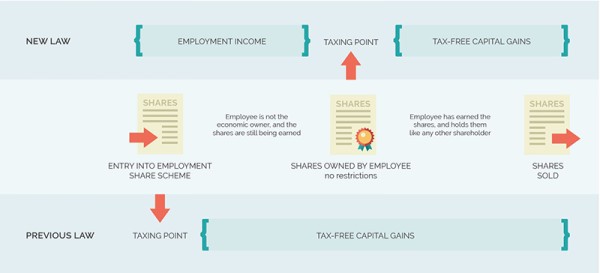

The biggest change in the rules is the point in time that the benefit is calculated. The value of a benefit under an employee share scheme is the amount by which the market value of the shares at the taxing point is more than the amount paid or payable for them. Under the old rules, the taxing point focused on when an interest in the shares was acquired, even if the shares had restricted rights or were unpaid at that date.

Under the new rules, the taxing point focuses on the “share scheme taxing date”.

The share scheme taxing date is the earlier of:

a. The date the benefits are either transferred or cancelled for consideration; or

b. The date the employee owns the shares in the same way as any other shareholder

Whether an employee owns the shares in the same way as any other shareholder depends on the terms of the scheme. An employee will not own the shares in the same way as any other shareholder if there is a material risk that the shares may be forfeited (i.e. good chance the shares will be forfeited). It is also likely this threshold will not be met if the employee does not have voting rights or entitlement to dividends for a period of time.

Generally, the new rules apply to benefits where the taxing point is after 29 September 2018. However, where shares were acquired between 12 May 2016 and 29 September 2018, the benefit will be taxable under the new rules if the taxing point is after 1 April 2022.

The new rules include agreements entered into before a person commences formal employment and covers shareholder- employees (to the extent PAYE is not deducted). However, the new rules do not apply to arrangements that require employees to pay market value for shares or to exempt employee share schemes (generally schemes offered to all or most employees), which have their own specific rules.

Stark Industries transfers shares worth $10,000 to a trustee on trust for its employee, Pepper Potts. If she leaves the company for any reason during the next three years, the shares are forfeited for nil consideration. If, after three years, Pepper is still with the company the shares will transfer to her.

Assuming that she does not leave the company, the taxing point will be at the end of the three year period. Pepper will be taxed on the value of the shares at that time.

In this example, there is a material risk that Pepper will leave the employment of Stark Industries (e.g. for a better opportunity). The taxing point does not occur while there is a material risk that the beneficial ownership of the shares will change.

Under the old rules, Pepper would likely have been taxed on the $10,000 value of the shares when they were transferred to the trust. Assuming the value of the company increases, the effect of the new rules is that the potential taxable benefit to Pepper will be at the highest point when it becomes taxable to her.

Stark Industries transfers shares worth $10,000 to a trustee on trust for its employee, Pepper Potts. She is not entitled to the shares unless particular performance hurdles are met. If the hurdle is met in year 1, one-third of the shares will vest. If it is met in year 2, a further one-third of the shares will vest. The same approach applies in year 3.

Vested shares are not transferred to Pepper but are held by the trustee until the three years are up. If she leaves before the three years are up, the vested shares will transfer to Pepper except if she is a bad leaver (i.e. leaves because of disciplinary action or misconduct).

Assuming that Pepper meets all her performance hurdles and does not leave the company, there will be a taxing point at the end of years 1, 2 and 3. She will be taxed at the end of each year on the value of the shares that vest at that time.

The likelihood that Pepper will be a bad leaver is low (i.e. not material) and so this condition will not defer the taxing point. The fact that the shares are held by a trustee until the end of year three will also not, in itself, defer the taxing point.

The terms of employee share schemes are wide and varied. If you are not sure of the share scheme taxing date under your employee share scheme or if you would like more information, please contact your usual Baker Tilly Staples Rodway advisor.

DISCLAIMER No liability is assumed by Baker Tilly Staples Rodway for any losses suffered by any person relying directly or indirectly upon any article within this website. It is recommended that you consult your advisor before acting on this information.

Our website uses cookies to help understand and improve your experience. Please let us know if that’s okay by you.

Cookies help us understand how you use our website, so we can serve up the right information here and in our other marketing.