Listed Property Trusts

A Listed Property Trust is a unitised portfolio of property assets, listed on a stock exchange. A listed property trust (LPT) usually invests in multiple buildings, has multiple tenants and generally owns a portfolio of large properties, which, due to their size and value, cannot be bought by the average private investor. These large investments are broken up into units of smaller value that can be purchased by private investors, who become shareholders. The minimum economic purchase amount is about $5,000.

Syndicated Property Property Syndicates enable you to invest in commercial, residential and industrial property by pooling your money with other investors. They typically offer higher returns but can be riskier than other forms of property investment. It’s also important to note that high returns aren’t guaranteed and your money will usually be locked in. The number of units available depends on the price paid for the property and you can buy more than one unit. The unit cost will vary but is typically about $50,000.

Returns

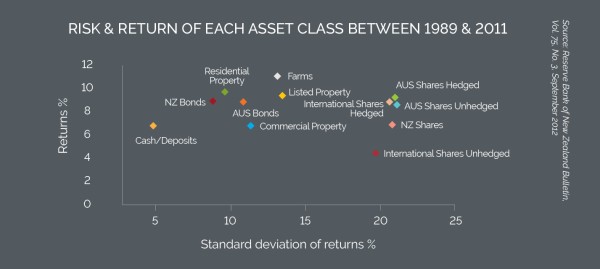

Listed Property Returns are linked to movements in the value of the properties and income generated by the property management companies. They potentially earn more than fixed interest and cash over the long term, but less than shares. Value tends to fluctuate more than fixed interest and cash but not shares, over time.

Syndicated Property Returns are based on the property’s rental income, minus the costs the syndicate has to pay. One of these costs will be for a property manager to take care of the management and maintenance of the property. As a part-owner of the property, you share responsibility for its costs and debts. These are divided by the number of units in the syndicate, and investors pay their share based on how many units they own. Investors in property syndicates pay fees to cover specialist services such as property management, legal and financial services. This can result in high fees that may increase even further over time. If there isn’t enough money in the syndicate pool to meet these obligations, you may need to invest more money and in some cases you’ll need to make this payment quite quickly. Your investment returns are not guaranteed and can vary. You should be aware that the return you receive on your investment may be different to the rate advertised by the property syndicate. Reasons for this include:

- tenants move out of the property and there is a delay finding new ones

- tenants can’t afford to pay their rent and outgoings

- the property manager or others involved in the syndicate increase their fees

- interest rates change and this affects the syndicate’s mortgage payments

- the property needs repairs or maintenance work

Risk & Liquidity

With Listed Property Trusts, you can sell out and get your money in 4 or 5 days for a brokerage rate of 0.75% to 1.5%. As with Property Syndicates you could end up selling for less than you paid however, provided you are properly diversified and hold for a reasonable time frame, that would be unusual.

Syndicated Property, unlike a bank term deposit where you can get your money back at the end of a set time period, property syndicates don’t usually have a fixed term. This can make it difficult to get your initial investment back if you need it, as there is no active market available for on-selling your investment when you want to exit. Syndicate managers don’t have to return your money if you need it, but they might help you sell your unit(s) to another investor. If you do this, you may have to pay fees. You may also have to sell them for less than you paid, especially if returns have dropped since you first invested. Otherwise you’ll need to wait until the property is sold, any loans repaid and the syndicate is wound up.

Diversification

With Listed Property Trusts you generally get the benefits of diversification lots of properties and diversified geographically. It is also fair to say that the quality of the buildings and the tenants of listed property is almost always of much higher quality than syndicates and, all things being equal, this means it is lower risk. One of the main benefits of listed property is that it can offer investors a good degree of diversification.

With syndicates you normally buy one property with a few tenants in one town in one sector and diversification may be rather limited.

Gearing

The average gearing of listed property trusts is between 25% and 35%.

Gearing on syndicated properties is frequently around 50%. High gearing (borrowing) equals higher risk.

Entry Costs

To buy a listed property trust on the stockmarket there is an average cost of 0.75% to 1.5% in brokerage.

The all-up fees for initial offerings of syndicated properties can be up to 10%.

This article does not seek to recommend one form of property investment over another, it is simply written to inform. Before you invest in any property or fund we recommend:

- You take advice from an experienced Authorised Financial Adviser (AFA).

- Understand your goals, objectives and do a risk profile.

- Consider not just property but a fully diversi-fied portfolio.

- Think about having it managed for you.

Staples Rodway Asset Management is a boutique investment advisory service, which deploys client capital in both passive and active strategies consistent with client objectives and risk profile. When adopting active investment management strategies Staples Rodway Asset Management seeks to identify managers that meet the criteria above. For further information on the services provided by Staples Rodway Asset Management, an Authorised Financial Adviser can be contacted on 0508 220 022 or enquiries@sraminvest.co.nz

SRAM was the investment division of the accounting firm Staples Rodway. In 2015 FANZ purchased a 50% shareholding in SRAM, and subsequently purchased the remaining 50% in 2018. The operations of SRAM and FANZ were combined in 2018 with the entities being formally amalgamated in 2019.

DISCLAIMER No liability is assumed by Baker Tilly Staples Rodway for any losses suffered by any person relying directly or indirectly upon any article within this website. It is recommended that you consult your advisor before acting on this information.